Stocks fell for a third consecutive week as the Middle East conflict continued to disrupt energy markets, bond yields climbed on inflation fears, and economic data offered only partial reassurance to rattled investors.

The Numbers

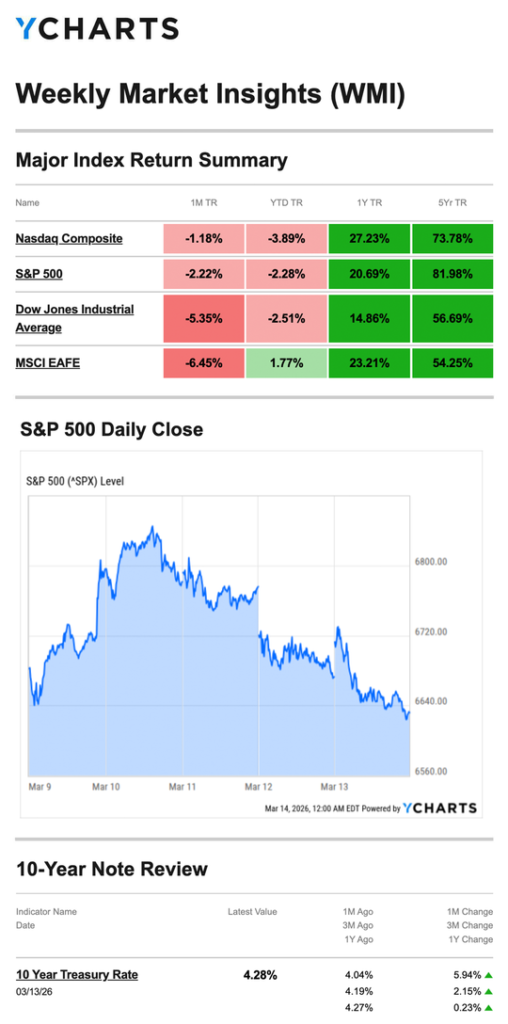

- S&P 500: −1.60%

- Nasdaq: −1.26%

- Dow Jones Industrial Average: −1.99%

- MSCI EAFE: −2.28%

Losses were broad across both U.S. and international markets, extending a difficult three-week stretch. The Dow has now underperformed the Nasdaq in each of the past two down weeks — an unusual pattern worth monitoring.

Source: YCharts.com, March 14, 2026. Weekly performance is measured from Monday, March 9, to Friday, March 13. TR = total return for the index, which includes any dividends and cash distributions during the period. Treasury note yield is expressed in basis points.

What Happened

Monday: Volatile Start, Late Recovery Stocks fell and oil prices rose as commercial maritime traffic through the Strait of Hormuz remained at a virtual standstill. Markets partially recovered late in the session after the White House suggested the conflict could end sooner than expected.

Tuesday–Wednesday: Coordinated Relief, Inflation Holds Steady Stocks dropped at Tuesday’s open before recovering on reports that the U.S. and other nations were weighing a coordinated release of strategic oil reserves to offset supply disruptions. Markets steadied midweek after Wednesday’s Consumer Price Index report showed inflation held flat in February year-over-year — a constructive data point that briefly steadied sentiment.

Thursday–Friday: Oil Hits Records, Growth Revised Lower The calm didn’t last. As the week progressed, oil prices closed at all-time highs and bond yields rose — reflecting investor concern that a prolonged conflict would keep energy prices elevated and reignite inflation pressure. The week closed with a downward revision to Q4 GDP adding to the cautious tone, though the pace of market declines slowed somewhat by Friday.

Inflation: Two Reports, Two Time Stamps Last week brought two inflation readings that tell slightly different stories — and it’s worth understanding the difference.

Wednesday’s CPI report showed consumer prices were flat in February compared to a year ago — welcome news. However, this data predates the Middle East conflict and the oil price surge that followed. Friday’s Personal Consumption Expenditures (PCE) index — the Fed’s preferred inflation gauge — showed consumer prices remained sticky in January, also before the conflict began. Markets largely looked past the PCE report given its age, but the underlying message is clear: inflation had not yet been fully tamed before this new supply shock arrived.

The next inflation readings will be the first to capture any pass-through from higher oil prices — and those will matter considerably more to the Fed.

What We’re Watching

This Week’s Fed Meeting: The Federal Reserve meets Tuesday and Wednesday, with the interest rate decision and Chair Powell’s press conference on Wednesday. This is the most consequential Fed meeting in months. Policymakers must now weigh persistent inflation, a weakening labor market, slowing growth, and an active geopolitical shock — all simultaneously. Markets will be listening closely for any shift in tone or forward guidance.

Oil and the Strait of Hormuz: The Strait of Hormuz remains the single most important variable for markets right now. A resolution — or even credible signs of one — could trigger a sharp reversal in both oil prices and equity sentiment. A prolonged standstill raises the risk of inflation re-acceleration and deeper economic disruption.

Wednesday’s PPI: The Producer Price Index arrives the same day as the Fed decision, offering the first upstream inflation read of the week. Combined with the rate decision, Wednesday is shaping up to be the most data-dense day of the quarter.

This Week’s Critical Data

- Wednesday: FOMC Interest Rate Decision; Fed Chair Press Conference; Producer Price Index (PPI)

- Thursday: Weekly Jobless Claims

Note: Several releases this week reflect data delayed by last year’s government shutdown.

Source: Investors Business Daily – Econoday economic calendar; March 13, 2026. Forecasts are subject to revision and may not materialize.

As always, if you have any questions about your portfolio or want to discuss your strategy, please don’t hesitate to reach out.

Crescent Private Wealth

Weekly Market Insights

Talk To Us!

Footnotes And Sources

WSJ.com, March 13, 2026

Investing.com, March 13, 2026

CNBC.com, March 9, 2026

CNBC.com, March 10, 2026

CNBC.com, March 11, 2026

WSJ.com, March 12, 2026

WSJ.com, March 13, 2026

CNBC.com, March 11, 2026

WSJ.com, March 13, 2026

IRS.gov, June 10, 2025