Stocks finished a choppy four-session week in positive territory, as tech-driven momentum proved resilient enough to overcome a slowing economy, sticky inflation, and fresh geopolitical friction.

The Numbers

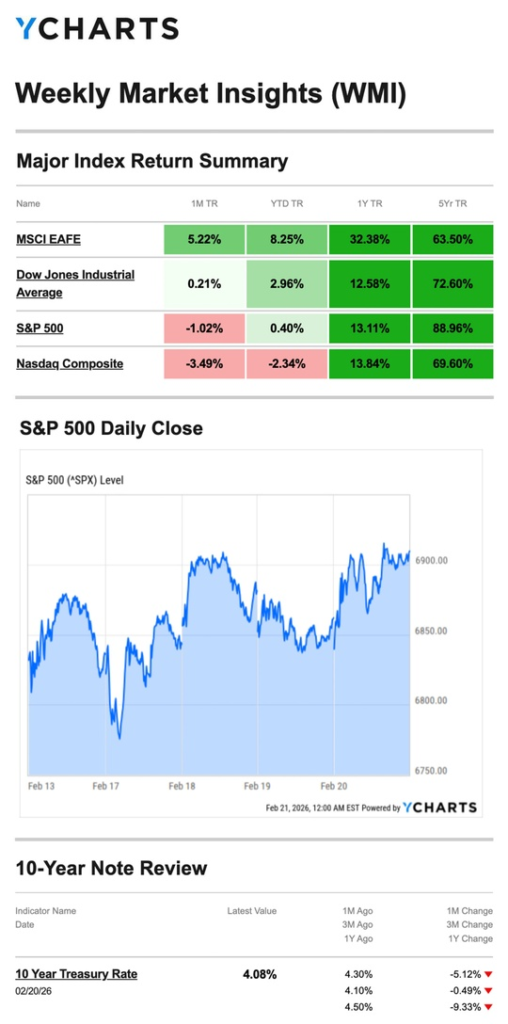

- S&P 500: +1.07%

- Nasdaq: +1.51%

- Dow Jones Industrial Average: +0.25%

- MSCI EAFE: +0.75%

Tech led the way, with the Nasdaq outpacing the broader market. All four major indexes finished in the green despite a week full of mixed signals.

Source: YCharts.com, February 21, 2026. Weekly performance is measured from Friday, February 13, to Friday, February 20. TR = total return for the index, which includes any dividends and cash distributions during the period. Treasury note yield is expressed in basis points.

What Happened

Early Week: Muted Start, Tech Builds Steam The shortened week opened quietly, with lingering AI disruption concerns in software keeping early gains modest. Momentum picked up as investors digested the Fed’s January meeting minutes, with tech broadly — including some lesser-known names — attracting renewed buying interest.

Mid-Week: Geopolitical Pressure Stocks pulled back as investors grew uneasy over rising tensions in the Middle East and concerns about stress in private credit markets within the financial sector.

Friday: Tariff Ruling Changes the Tone Markets rallied to close the week after the Supreme Court struck down the White House’s tariffs. The ruling itself had been widely anticipated — but the timing caught investors off guard, and the news was welcomed. Without tariffs in place, companies may have greater pricing flexibility, a potential tailwind for margins.

The tariff news overshadowed two softer economic releases that arrived the same morning:

- Inflation remained sticky, with the data offering little reassurance that the Fed’s 2% target is close at hand.

- Q4 GDP came in at 1.4% growth — well below the 2.5% expected and a sharp deceleration from Q3’s 4.4% pace. The slowdown was driven by declines in both federal and consumer spending, with the government shutdown weighing on the federal side.

What We’re Watching

Growth Slowing, but Markets Looking Past It Friday’s GDP miss was significant — cutting the growth rate nearly in half from Q3 — yet markets rallied anyway. This suggests investors are currently more focused on policy tailwinds (the tariff ruling, potential rate cuts) than on near-term growth softness. That calculus could shift if weak data continues to accumulate.

Fed Speakers in Focus This Week With no major Fed meeting until March, a heavy lineup of Fed officials speaking this week offers the next best window into how policymakers are reading the current mix of slowing growth and persistent inflation.

Inflation Still the Wildcard Sticky inflation data, combined with softer growth, puts the Fed in a difficult position. Markets will be closely watching Friday’s Producer Price Index for January to see whether upstream price pressures are easing.

This Week’s Critical Data

- Tuesday: Consumer Confidence

- Friday: Producer Price Index (PPI) — January

Source: Investors Business Daily – Econoday economic calendar; February 20, 2026. Forecasts are subject to revision and may not materialize.

As always, if you have any questions about your portfolio or want to discuss your strategy, please don’t hesitate to reach out.

Crescent Private Wealth

Weekly Market Insights

Talk To Us!

Footnotes And Sources

WSJ.com, February 20, 2026

Investing.com, February 20, 2026

CNBC.com, February 17, 2026

CNBC.com, February 17, 2026

CNBC.com, February 19, 2026

WSJ.com, February 20, 2026

WSJ.com, February 20, 2026

IRS.gov, May 29, 2025

Investing involves risks, and investment decisions should be based on your own goals, time horizon, and tolerance for risk. The return and principal value of investments will fluctuate as market conditions change. When sold, investments may be worth more or less than their original cost.

The forecasts or forward-looking statements are based on assumptions, may not materialize, and are subject to revision without notice.

The market indexes discussed are unmanaged, and generally, considered representative of their respective markets. Index performance is not indicative of the past performance of a particular investment. Indexes do not incur management fees, costs, and expenses. Individuals cannot directly invest in unmanaged indexes. Past performance does not guarantee future results.

The Dow Jones Industrial Average is an unmanaged index that is generally considered representative of large-capitalization companies on the U.S. stock market. The Nasdaq Composite is an index of the common stocks and similar securities listed on the Nasdaq stock market and considered a broad indicator of the performance of stocks of technology and growth companies. The MSCI EAFE Index was created by Morgan Stanley Capital International (MSCI) and serves as a benchmark of the performance of major international equity markets, as represented by 21 major MSCI indexes from Europe, Australia, and Southeast Asia. The S&P 500 Composite Index is an unmanaged group of securities that are considered to be representative of the stock market in general.

U.S. Treasury Notes are guaranteed by the federal government as to the timely payment of principal and interest. However, if you sell a Treasury Note prior to maturity, it may be worth more or less than the original price paid. Fixed income investments are subject to various risks including changes in interest rates, credit quality, inflation risk, market valuations, prepayments, corporate events, tax ramifications and other factors.

International investments carry additional risks, which include differences in financial reporting standards, currency exchange rates, political risks unique to a specific country, foreign taxes and regulations, and the potential for illiquid markets. These factors may result in greater share price volatility.