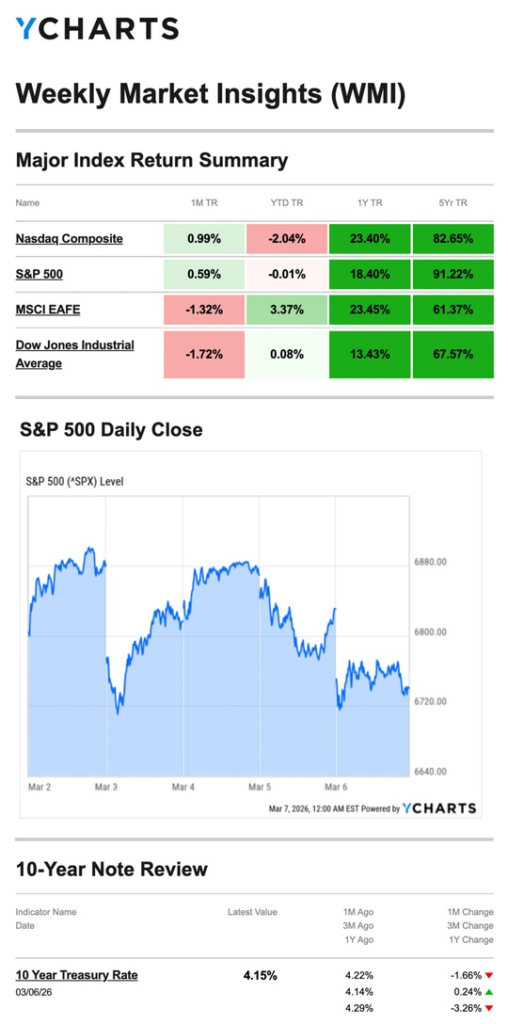

Stocks fell last week as a new Middle East conflict rattled global markets, a surprise jobs loss unsettled investors, and surging oil prices added a new layer of economic uncertainty to an already complicated environment.

The Numbers

- S&P 500: −2.02%

- Nasdaq: −1.24%

- Dow Jones Industrial Average: −3.05%

- MSCI EAFE: −6.62%

The losses were broad and significant — but the international number stands out. Developed overseas markets fell more than three times as sharply as U.S. equities, reflecting the geographic proximity of the conflict and Europe’s greater energy dependency.

Source: YCharts.com, March 7, 2026. Weekly performance is measured from Monday, March 2, to Friday, March 6. TR = total return for the index, which includes any dividends and cash distributions during the period. Treasury note yield is expressed in basis points.

What Happened

Monday: Conflict Breaks, Markets Dip and Recover Stocks opened lower as investors reacted to news of military action in the Middle East. The selloff was contained, however, as buyers stepped in quickly. All three major averages recovered or nearly recovered their intraday losses by the close.

Tuesday: Partial Recovery on Policy Reassurance Markets opened lower again as investors weighed the possibility of a prolonged conflict. Afternoon comments from the White House — announcing plans to provide risk insurance and U.S. Navy escorts for oil tankers and commercial vessels in the Persian Gulf — helped stabilize sentiment, and stocks partially recovered before the close.

Wednesday: Brief Window of Optimism Equities opened higher Wednesday, lifted by a tech rebound, stabilizing oil prices, and a stronger-than-expected ADP private payrolls report. By the closing bell, both the S&P 500 and Nasdaq had turned positive for the week.

Thursday–Friday: Pressure Returns The recovery proved short-lived. Markets resumed their decline on concerns about a widening conflict. Friday’s official jobs report from the Bureau of Labor Statistics delivered an unexpected blow: the economy lost 92,000 jobs last month, a stark reversal from recent trends. News that some Middle Eastern oil fields had begun cutting production amid limited storage capacity added further complexity to an already tense market environment..

Oil: The Economic Wildcard U.S. crude oil prices surged 36% last week — the largest single-week gain since 1983. The conflict has brought tanker traffic through the Strait of Hormuz, one of the world’s most critical energy shipping routes, to a near standstill. Beyond the immediate price shock, markets are watching how insurers respond: if risk premiums on maritime shipping rise sharply in the coming weeks, the cost of moving energy and goods globally could climb alongside them.

Rising oil prices function as a tax on consumers and businesses alike, and a sustained spike would complicate the Fed’s already delicate balancing act between slowing growth and stubborn inflation.

What We’re Watching

The Conflict’s Economic Reach Last week demonstrated how quickly a geopolitical shock can ripple through energy markets, employment sentiment, and global equities. The duration and scope of the conflict will be the dominant variable for markets in the near term.

A Jobs Market That Just Flipped Losing 92,000 jobs in a single month is a significant data point — especially following recent months of mixed but generally positive labor trends. Whether this is a one-month anomaly or the beginning of a broader deterioration will be a central question for investors and the Fed alike.

A Pivotal Friday Ahead This Friday brings a compressed but consequential data release: Q4 GDP, the PCE inflation index, durable goods, job openings, and consumer sentiment — several of which were delayed by last year’s government shutdown. Taken together, they will offer the most complete snapshot of the economy’s pre-conflict baseline.

This Week’s Critical Data

- Wednesday: Consumer Price Index (CPI)

- Friday: Q4 GDP (first revision); PCE Index; Consumer Sentiment

Note: Several Friday releases reflect data delayed by last year’s government shutdown. Source: Investors Business Daily – Econoday economic calendar; March 6, 2026. Forecasts are subject to revision and may not materialize.

As always, if you have any questions about your portfolio or want to discuss your strategy, please don’t hesitate to reach out.

Crescent Private Wealth

Weekly Market Insights

Talk To Us!

Footnotes And Sources

WSJ.com, March 6, 2026

Investing.com, March 6, 2026

CNBC.com, March 2, 2026

CNBC.com, March 3, 2026

CNBC.com, March 4, 2026

WSJ.com, March 5, 2026

WSJ.com, March 6, 2026

CNBC.com, March 6, 2026

IRS.gov, July 8, 2025