Markets endured another turbulent week as rapid-fire developments in the Middle East conflict whipsawed investor sentiment, leaving stocks lower for a fourth consecutive week despite brief stretches of optimism early on.

The Numbers

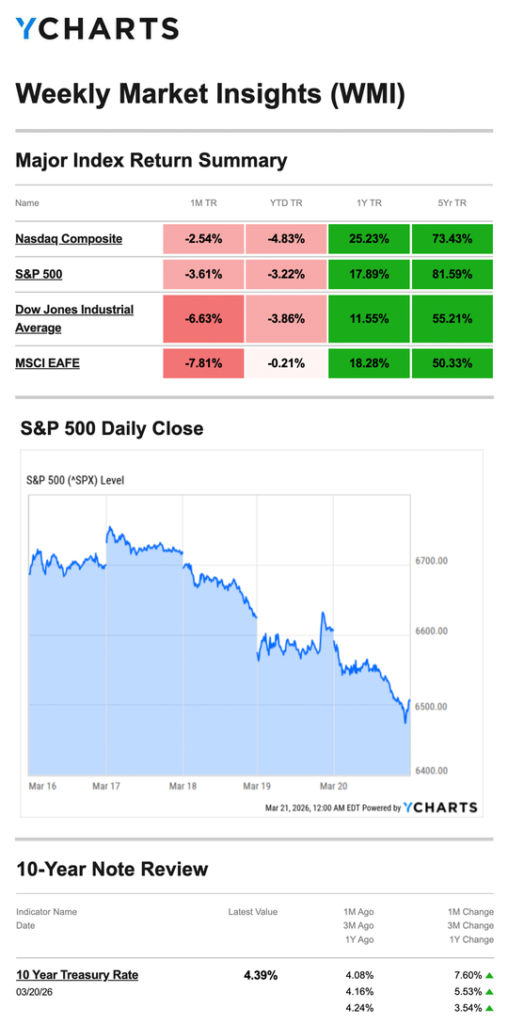

- S&P 500: −1.89%

- Nasdaq: −2.07%

- Dow Jones Industrial Average: −2.11%

- MSCI EAFE: −2.01%

For the first time in several weeks, U.S. and international markets fell in near-lockstep — a sign that the conflict’s economic implications are being felt broadly across global equity markets, not just domestically.

Source: YCharts.com, March 21, 2026. Weekly performance is measured from Monday, March 16, to Friday, March 20. TR = total return for the index, which includes any dividends and cash distributions during the period. Treasury note yield is expressed in basis points.

What Happened

Monday–Tuesday: Cautious Rebound Stocks opened the week higher as oil prices eased and investors saw potential value in beaten-down names. Reports that a coalition of countries was considering joining efforts to escort tankers out of the Persian Gulf provided an additional lift. Markets held their footing Tuesday as investors awaited further conflict developments, largely looking past fresh attacks on tanker ships near the Strait of Hormuz — the chokepoint through which roughly one in five barrels of the world’s exported oil passes.

Wednesday: Fed Holds, Inflation Bites The Federal Reserve held rates steady at its 3.50%–3.75% target range, as expected. But the accompanying tone was less reassuring than markets had hoped. Fed Chair Powell acknowledged that inflation was not declining as quickly as policymakers had projected. Separately, a warmer-than-expected wholesale inflation reading added to the pressure, and stocks resumed their decline.

Thursday: Slide Continues, Late Rally Cushions Stocks fell again Thursday as optimism about a near-term reopening of the Strait of Hormuz began to fade. A late-session relief rally helped limit the day’s losses but did little to change the week’s direction.

Friday: Iran Declares Force Majeure Stocks opened lower and briefly stabilized midday — before Iran declared force majeure on all foreign-owned oilfields, a significant escalation that sent markets lower again into the close. It was a fitting end to a week defined by headlines arriving faster than investors could process them.

The Fed’s Message This Week While the rate decision itself was widely anticipated, the Fed’s tone deserves attention. Chair Powell’s acknowledgment that inflation is proving more stubborn than projected — combined with the so-called dot plot showing a possible rate adjustment before year-end — signals that the Fed is navigating a genuinely difficult environment. Policymakers are contending with slowing growth, a labor market showing cracks, and now an energy price shock that could push inflation higher before it moves lower. The Fed appears to be holding its ground for now, but the margin for error is narrowing.

What We’re Watching

Iran’s Force Majeure Declaration Friday’s late-session escalation is the most significant development to monitor heading into this week. A force majeure on foreign-owned oilfields could meaningfully reduce global oil supply and keep energy prices elevated — deepening the inflationary pressure the Fed is already struggling to contain.

Four Down Weeks U.S. equities have now declined four consecutive weeks. While that alone doesn’t signal a sustained bear market, the combination of geopolitical shock, sticky inflation, slowing growth, and a Fed with limited room to maneuver creates a more challenging environment than markets faced entering the year.

A Quieter Data Week This week’s economic calendar is relatively light, with Friday’s final Consumer Sentiment reading the most watched release. That puts the Middle East squarely back in the driver’s seat as the primary market catalyst.

This Week’s Critical Data

- Tuesday: PMI — Manufacturing and Services

- Friday: Consumer Sentiment (final)

Some releases this week reflect data delayed by last year’s government shutdown. Source: Investors Business Daily – Econoday economic calendar; March 20, 2026. Forecasts are subject to revision and may not materialize.

As always, if you have any questions about your portfolio or want to discuss your strategy, please don’t hesitate to reach out.

Crescent Private Wealth

Weekly Market Insights

Talk To Us!

Footnotes And Sources

WSJ.com, March 20, 2026

Investing.com, March 20, 2026

CNBC.com, March 16, 2026

CNBC.com, March 17, 2026

WSJ.com, March 18, 2026

CNBC.com, March 19, 2026

CNBC.com, March 19, 2026

WSJ.com, March 18, 2026

IRS.gov, September 24, 2025

Investing involves risks, and investment decisions should be based on your own goals, time horizon, and tolerance for risk. The return and principal value of investments will fluctuate as market conditions change. When sold, investments may be worth more or less than their original cost.

The forecasts or forward-looking statements are based on assumptions, may not materialize, and are subject to revision without notice.

The market indexes discussed are unmanaged, and generally, considered representative of their respective markets. Index performance is not indicative of the past performance of a particular investment. Indexes do not incur management fees, costs, and expenses. Individuals cannot directly invest in unmanaged indexes. Past performance does not guarantee future results.

The Dow Jones Industrial Average is an unmanaged index that is generally considered representative of large-capitalization companies on the U.S. stock market. The Nasdaq Composite is an index of the common stocks and similar securities listed on the Nasdaq stock market and considered a broad indicator of the performance of stocks of technology and growth companies. The MSCI EAFE Index was created by Morgan Stanley Capital International (MSCI) and serves as a benchmark of the performance of major international equity markets, as represented by 21 major MSCI indexes from Europe, Australia, and Southeast Asia. The S&P 500 Composite Index is an unmanaged group of securities that are considered to be representative of the stock market in general.

U.S. Treasury Notes are guaranteed by the federal government as to the timely payment of principal and interest. However, if you sell a Treasury Note prior to maturity, it may be worth more or less than the original price paid. Fixed income investments are subject to various risks including changes in interest rates, credit quality, inflation risk, market valuations, prepayments, corporate events, tax ramifications and other factors.

International investments carry additional risks, which include differences in financial reporting standards, currency exchange rates, political risks unique to a specific country, foreign taxes and regulations, and the potential for illiquid markets. These factors may result in greater share price volatility.