Stocks fell for a fifth consecutive week as early optimism around ceasefire talks gave way to deeper concern about the lasting economic damage of a prolonged conflict — and the Nasdaq and Dow both slipped into correction territory by Friday’s close.

The Numbers

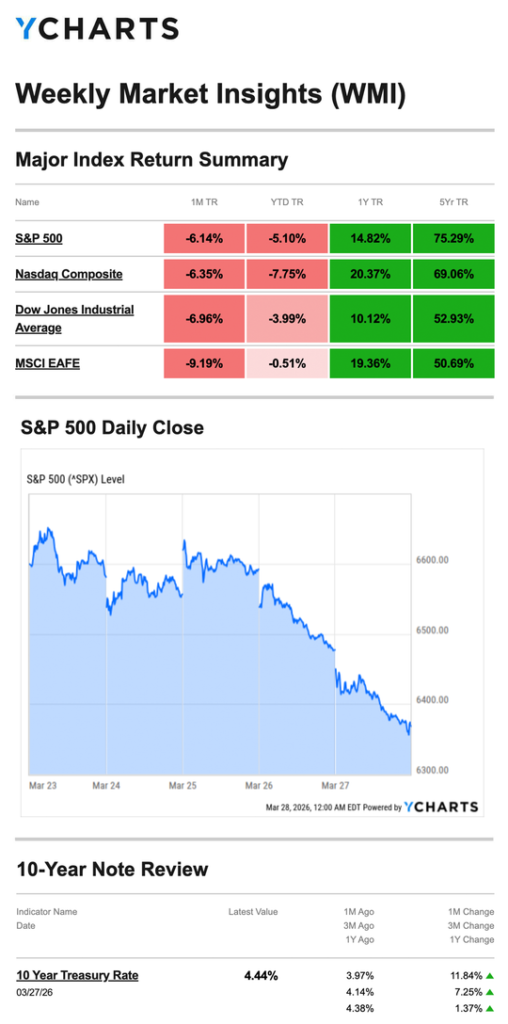

- S&P 500: −2.12%

- Nasdaq: −3.23%

- Dow Jones Industrial Average: −0.90%

- MSCI EAFE: −0.05%

The divergence within U.S. markets is notable: the Nasdaq bore the brunt of the week’s selling while the Dow held up comparatively well. International developed markets were essentially flat, suggesting overseas investors may be finding some footing even as U.S. equities continue to slide.

Source: YCharts.com, March 28, 2026. Weekly performance is measured from Monday, March 23, to Friday, March 27. TR = total return for the index, which includes any dividends and cash distributions during the period. Treasury note yield is expressed in basis points.

What Happened

Monday: Best Day Since February Markets opened with genuine optimism as ceasefire hopes resurfaced and Iran’s force majeure declaration appeared to produce no immediate further escalation. The White House described diplomatic conversations as “very good and productive.” Both the Dow and S&P 500 posted their strongest single-day gains since early February.

Tuesday–Wednesday: Recovery on Mediation Reports Stocks came under pressure Tuesday before rebounding Wednesday on reports that Pakistan was actively mediating ceasefire talks. All three major averages posted solid midweek gains, though trading volumes suggested retail investors remained largely on the sidelines — a sign that conviction behind the rally was limited.

Thursday–Friday: Optimism Fades, Selling Accelerates The mood shifted again Thursday as markets fell despite a White House announcement after the close that it was extending its pause on military strikes against Iranian energy infrastructure by an additional 10 days. The extension did little to reassure investors. Selling intensified Friday, with the Nasdaq and Dow both falling into correction territory — defined as a decline of 10% or more from a recent peak. The S&P 500 recorded its longest weekly losing streak in nearly four years.

Sector Spotlight: Energy Stands Apart While most of the market has struggled, energy stocks have been a notable exception. By Friday’s close, 19 energy companies in the S&P 500 were trading at 52-week highs — a direct reflection of elevated oil prices and the supply uncertainty that continues to grip global energy markets. For investors with energy exposure in their portfolios, this has been a rare source of resilience during a difficult stretch.

What We’re Watching

Five Down Weeks — and a Correction The S&P 500’s five-week losing streak is now the longest in nearly four years. With the Nasdaq and Dow in correction territory, the question investors are asking is whether this is a painful but temporary geopolitical disruption or the beginning of a more sustained repricing of risk. The answer likely depends heavily on how quickly the Middle East situation resolves.

A Heavy Week for Data and Fed Voices This week’s calendar is among the busiest of the year, with the Friday Employment Report as the centerpiece. Given last month’s unexpected job loss of 92,000, another weak reading could meaningfully shift the Fed’s calculus. A heavy lineup of Fed officials speaking throughout the week will also be closely watched for any signals that the central bank is reconsidering its current stance.

Wednesday’s Retail Sales and ADP Two mid-week releases — retail sales and the ADP private payrolls report — will offer an early read on whether consumer spending and hiring held up through February before the conflict intensified.

This Week’s Critical Data

- Wednesday: Retail Sales (February, delayed); ADP Employment Report

- Friday: Employment Report; PMI — Services

Several releases this week reflect data delayed by last year’s government shutdown.

Source: Investors Business Daily – Econoday economic calendar; March 27, 2026. Forecasts are subject to revision and may not materialize.

As always, if you have any questions about your portfolio or want to discuss your strategy, please don’t hesitate to reach out.

Crescent Private Wealth

Weekly Market Insights

Talk To Us!

Footnotes And Sources

WSJ.com, March 27, 2026

Investing.com, March 27, 2026

CNBC.com, March 16, 2026

CNBC.com, March 24, 2026

WSJ.com, March 27, 2026

CNBC.com, March 19, 2026

IRS.gov, June 23, 2025