Stocks were mixed last week as investors navigated a ceasefire extension, new all-time highs in the S&P 500 and Nasdaq, and a striking disconnect between what consumers are saying and what they are actually doing.

The Numbers

- S&P 500: +0.55%

- Nasdaq: +1.50%

- Dow Jones Industrial Average: −0.44%

- MSCI EAFE: −2.75%

U.S. large-cap and tech indexes pushed higher while the Dow lagged and international developed markets pulled back notably — a reminder that the conflict’s ripple effects continue to land unevenly across global markets.

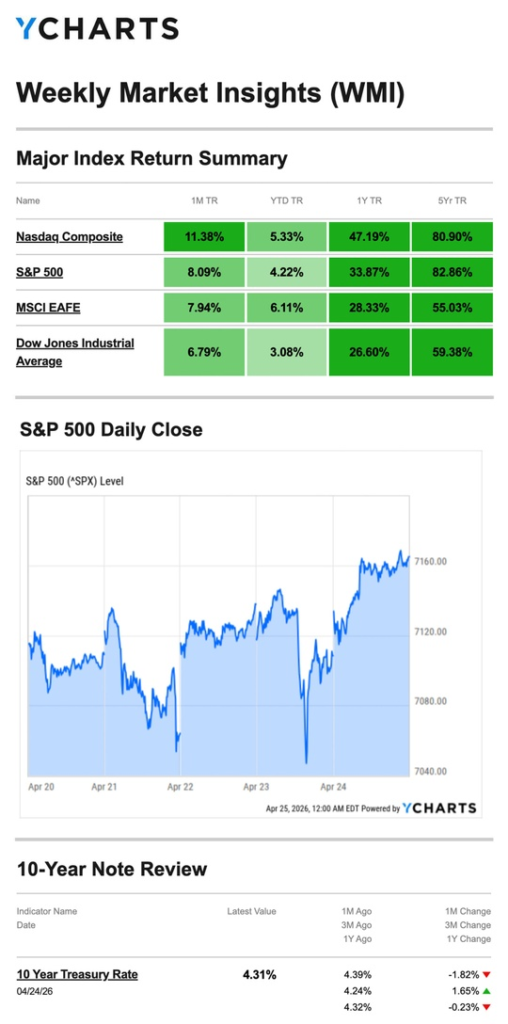

Source: YCharts.com, April 25, 2026. Weekly performance is measured from Monday, April 20, to Friday, April 24. TR = total return for the index, which includes any dividends and cash distributions during the period. Treasury note yield is expressed in basis points.

What Happened

Monday–Tuesday: Ceasefire Anxiety Stocks opened the week lower after weekend escalations in the Middle East renewed tensions. Markets stayed under pressure through Tuesday’s close as investors braced for Wednesday’s ceasefire expiration deadline — uncertain whether an extension would materialize.

Wednesday: Extension Confirmed, New Highs Reached Relief arrived Wednesday morning when a ceasefire extension was announced. Combined with solid first-quarter corporate earnings results, the news drove all three major averages higher. Oil climbed back above $100 per barrel, but that did little to dampen equity enthusiasm — the S&P 500 and Nasdaq both closed at new all-time highs.

Thursday–Friday: Desensitization Sets In Markets absorbed a slump in software stocks and continued oil price pressure without significant damage, logging fresh intraday highs along the way. Investors appeared increasingly willing to look past Middle East headlines — a notable shift from the hair-trigger sensitivity that defined markets just a few weeks ago.

The Consumer Paradox Friday brought one of the more puzzling data combinations of the year: consumer sentiment fell to an all-time low in April, yet last Tuesday’s retail sales report showed consumer spending rose 1.7% in March — the largest monthly increase in more than three years.

Consumers, it seems, are anxious but still spending. The sentiment reading likely reflects genuine worry about inflation, job security, and geopolitical uncertainty. The spending data suggests those concerns haven’t yet translated into behavioral change at the checkout counter. The question for markets — and for the Fed — is which of these signals is the more reliable leading indicator of where the economy is headed.

What We’re Watching

A Consequential Week Ahead This week may be the most data-dense of the year. Wednesday brings the FOMC interest rate decision and Chair Powell’s press conference — the Fed’s first opportunity to formally respond to the conflict’s economic fallout, the inflation spike, and signs of consumer strain. Thursday adds Q1 GDP, the PCE inflation index, and the Employment Cost Index. Taken together, this week will provide the most complete read yet on whether the U.S. economy is weathering this period of turbulence or beginning to bend under it.

The Fed’s Difficult Balance With headline inflation elevated, consumer sentiment at historic lows, and spending still holding up, the Fed faces a genuinely difficult call. Markets will be listening closely for any signal about the pace and timing of future rate moves — and Powell’s press conference tone will matter as much as the decision itself.

Oil Above $100 Oil crossing back above $100 per barrel is a psychological and economic threshold worth watching. If it holds or climbs further, the transitory inflation narrative becomes harder to sustain — and the Fed’s room to maneuver narrows further.

This Week’s Critical Data

- Wednesday: FOMC Interest Rate Decision; Fed Chair Press Conference

- Thursday: Q1 GDP; PCE Index; Employment Cost Index; Weekly Jobless Claims

Note: Some releases this week reflect data delayed by last year’s government shutdown. Source: Investors Business Daily – Econoday economic calendar; April 24, 2026. Forecasts are subject to revision and may not materialize.

As always, if you have any questions about your portfolio or want to discuss your strategy, please don’t hesitate to reach out.

Crescent Private Wealth

Weekly Market Insights

Talk To Us!

Footnotes And Sources

WSJ.com, April 17, 2026

Investing.com, April 24, 2026

CNBC.com, April 21, 2026

CNBC.com, April 22, 2026

CNBC.com, April 23, 2026

WSJ.com, April 24, 2026

CNBC.com, April 24, 2026

WSJ.com, April 21, 2026

IRS.gov, January 17, 2025

Investing involves risks, and investment decisions should be based on your own goals, time horizon, and tolerance for risk. The return and principal value of investments will fluctuate as market conditions change. When sold, investments may be worth more or less than their original cost.

The forecasts or forward-looking statements are based on assumptions, may not materialize, and are subject to revision without notice.

The market indexes discussed are unmanaged, and generally, considered representative of their respective markets. Index performance is not indicative of the past performance of a particular investment. Indexes do not incur management fees, costs, and expenses. Individuals cannot directly invest in unmanaged indexes. Past performance does not guarantee future results.

The Dow Jones Industrial Average is an unmanaged index that is generally considered representative of large-capitalization companies on the U.S. stock market. The Nasdaq Composite is an index of the common stocks and similar securities listed on the Nasdaq stock market and considered a broad indicator of the performance of stocks of technology and growth companies. The MSCI EAFE Index was created by Morgan Stanley Capital International (MSCI) and serves as a benchmark of the performance of major international equity markets, as represented by 21 major MSCI indexes from Europe, Australia, and Southeast Asia. The S&P 500 Composite Index is an unmanaged group of securities that are considered to be representative of the stock market in general.

U.S. Treasury Notes are guaranteed by the federal government as to the timely payment of principal and interest. However, if you sell a Treasury Note prior to maturity, it may be worth more or less than the original price paid. Fixed income investments are subject to various risks including changes in interest rates, credit quality, inflation risk, market valuations, prepayments, corporate events, tax ramifications and other factors.

International investments carry additional risks, which include differences in financial reporting standards, currency exchange rates, political risks unique to a specific country, foreign taxes and regulations, and the potential for illiquid markets. These factors may result in greater share price volatility.