Stocks edged higher last week as initial inflation anxiety gave way to relief that the numbers met expectations, while Middle East diplomatic progress and the largest IPO in history added fuel to a cautiously optimistic close.

The Numbers

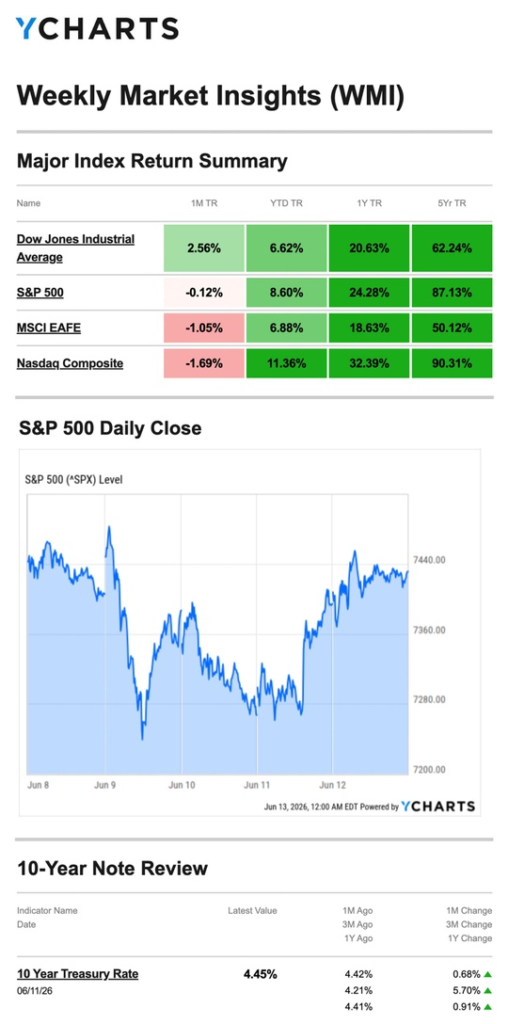

- S&P 500: +0.65%

- Nasdaq: +0.70%

- Dow Jones Industrial Average: +0.66%

- MSCI EAFE: +0.92%

Gains were notably uniform across all four indexes — a sign of broad, if modest, participation. International developed markets led slightly, continuing their pattern of quiet resilience throughout the conflict period.

Source: YCharts.com, June 13, 2026. Weekly performance is measured from Monday, June 8, to Friday, June 12. TR = total return for the index, which includes any dividends and cash distributions during the period. Treasury note yield is expressed in basis points.

What Happened

Monday: Chips Lead, Dow Lags

The week opened mixed. Chip stocks drove gains in the S&P 500 and Nasdaq while the Dow sagged, reflecting the familiar split between growth-oriented and economically sensitive sectors.

Tuesday: Script Flips

The rotation reversed the following session. Chip stocks fizzled despite a drop in oil prices, while the Dow gained as materials, consumer discretionary, and real estate sectors led. Real estate stocks rose on better-than-expected existing home sales — a welcome data point for a sector that has struggled under elevated rate expectations.

Wednesday: CPI Lands, Markets Sell Off

Stocks fell broadly after the May Consumer Price Index showed year-over-year inflation climbing to 4.2% — a three-year high. The initial reaction was negative, though as investors dug into the details, the picture became more nuanced.

Thursday: Diplomacy Steadies Sentiment

Markets recovered after the White House provided an update on ongoing Middle East diplomatic efforts, reviving optimism that a peace deal remains within reach. The geopolitical narrative continues to function as a meaningful counterweight to macro headwinds.

Friday: Record IPO Closes the Week on a High Note

The week ended positively as the largest IPO on record generated broad investor enthusiasm — particularly around AI — and further Middle East updates kept the diplomatic momentum alive.

Inflation: A Closer Look at the Numbers

Headline CPI rising to 4.2% year-over-year, a three-year high, sounds alarming. But Wall Street found enough context in the details to avoid a repeat of last week’s sharp selloff.

Three factors shaped the relatively measured reaction. First, the 4.2% reading matched market expectations exactly, removing the element of surprise that tends to drive the sharpest moves. Second, core inflation, which strips out energy and food prices, rose 2.9% year-over-year, also in line with forecasts and meaningfully lower than the headline number. Third, month-over-month CPI cooled slightly, giving investors tentative hope that energy prices may be approaching a peak.

The energy-driven gap between headline and core inflation remains the central story. If oil prices stabilize or decline as the Middle East situation resolves, headline inflation could fall back toward core relatively quickly. If energy remains elevated, the pressure on the Fed intensifies.

What We’re Watching

Wednesday’s Fed Decision — Chair Warsh’s First

This is the week’s defining event. Wednesday brings the FOMC interest rate decision and, critically, the first press conference of Kevin Warsh’s tenure as Fed Chair. With inflation at a three-year high, a labor market running hot, and markets on edge, Warsh’s tone and forward guidance will be parsed closely. A rate hike this week would be a significant market shock; holding steady with hawkish language would be more manageable but still consequential. Either way, this press conference will set the tone for the second half of 2026.

Retail Sales on Wednesday

Arriving the same day as the Fed decision, May retail sales will offer a read on whether consumers are beginning to pull back under the weight of higher energy costs and inflation. A soft number ahead of the Fed announcement could complicate the market’s reaction to whatever Warsh signals.

Markets Close Friday for Juneteenth

This is a four-day trading week. With the Fed decision on Wednesday and jobless claims on Thursday, the week’s key information will be fully absorbed by Thursday’s close, giving investors a long weekend to process before trading resumes Monday.

This Week’s Critical Data

- Wednesday: FOMC Interest Rate Decision; Fed Chair Warsh Press Conference; Retail Sales

- Thursday: Weekly Jobless Claims

Note: Markets are closed Friday, June 19, in observance of Juneteenth.

Source: Investors Business Daily – Econoday economic calendar; June 12, 2026. Forecasts are subject to revision and may not materialize.

As always, if you have any questions about your portfolio or want to discuss your strategy, please don’t hesitate to reach out.

Crescent Private Wealth

Weekly Market Insights

Talk To Us!

Footnotes And Sources

WSJ.com, June 12, 2026

Investing.com, June 12, 2026

CNBC.com, June 8, 2026

CNBC.com, June 9, 2026

WSJ.com, June 10, 2026

CNBC.com, June 11, 2026

CNBC.com, June 12, 2026

WSJ.com, June 10, 2026

Investing involves risks, and investment decisions should be based on your own goals, time horizon, and tolerance for risk. The return and principal value of investments will fluctuate as market conditions change. When sold, investments may be worth more or less than their original cost.

The forecasts or forward-looking statements are based on assumptions, may not materialize, and are subject to revision without notice.

The market indexes discussed are unmanaged, and generally, considered representative of their respective markets. Index performance is not indicative of the past performance of a particular investment. Indexes do not incur management fees, costs, and expenses. Individuals cannot directly invest in unmanaged indexes. Past performance does not guarantee future results.

The Dow Jones Industrial Average is an unmanaged index that is generally considered representative of large-capitalization companies on the U.S. stock market. The Nasdaq Composite is an index of the common stocks and similar securities listed on the Nasdaq stock market and considered a broad indicator of the performance of stocks of technology and growth companies. The MSCI EAFE Index was created by Morgan Stanley Capital International (MSCI) and serves as a benchmark of the performance of major international equity markets, as represented by 21 major MSCI indexes from Europe, Australia, and Southeast Asia. The S&P 500 Composite Index is an unmanaged group of securities that are considered to be representative of the stock market in general.

U.S. Treasury Notes are guaranteed by the federal government as to the timely payment of principal and interest. However, if you sell a Treasury Note prior to maturity, it may be worth more or less than the original price paid. Fixed income investments are subject to various risks including changes in interest rates, credit quality, inflation risk, market valuations, prepayments, corporate events, tax ramifications and other factors.

International investments carry additional risks, which include differences in financial reporting standards, currency exchange rates, political risks unique to a specific country, foreign taxes and regulations, and the potential for illiquid markets. These factors may result in greater share price volatility.