Stocks posted solid gains over a shortened holiday week as Middle East diplomatic momentum carried markets higher early, a weaker-than-expected jobs report recalibrated rate hike fears, and the Dow closed at a fresh record to end the period.

The Numbers

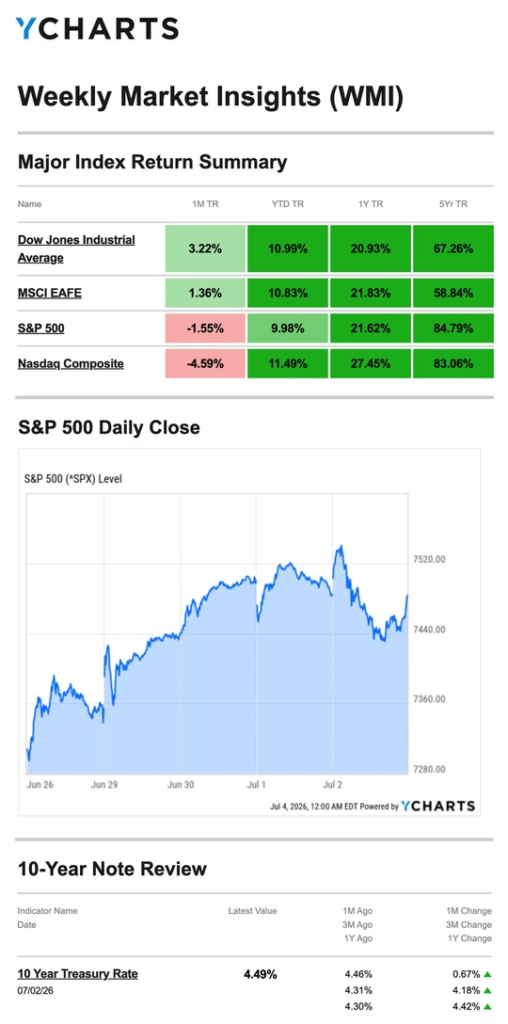

- S&P 500: +1.77%

- Nasdaq: +2.12%

- Dow Jones Industrial Average: +1.97%

- MSCI EAFE: +1.81%

Gains were broad and remarkably uniform across all four indexes — a sign of genuine market-wide participation rather than narrow leadership. The Dow’s record close capped a strong two-week stretch for cyclical and value-oriented names.

Source: YCharts.com, July 4, 2026. Weekly performance is measured from Friday, June 26, to Thursday, July 2. TR = total return for the index, which includes any dividends and cash distributions during the period. Treasury note yield is expressed in basis points.

What Happened

Monday: Diplomacy Drives the Open

Stocks climbed out of the gate on weekend news about U.S.-Iran relations, extending the constructive tone that has followed the peace agreement announcement. Broad gains across all three major averages set a positive tone for the week.

Tuesday: Chips Take the Lead

The rally narrowed on the second session, with semiconductor stocks driving outsized gains. The Nasdaq surged more than 3.5%, and the S&P 500 rose roughly 2% over the first two days of the week combined, a strong two-day start to what would become a holiday-shortened stretch.

Wednesday: Rotation Kicks In as July Begins

As the calendar turned to July, investors rotated out of AI and tech names. The Dow hit a new intraday high before pulling back slightly. The S&P 500 and Nasdaq declined on the session, though company-specific positive news for a handful of megacap tech names limited the downside.

Thursday: Jobs Miss, Markets Turn Mixed

Stocks initially rallied after the June jobs report came in well below expectations, a softer labor-market reading that investors interpreted as reducing the likelihood of a near-term Fed rate hike. However, as the session progressed, markets turned more mixed heading into the long holiday weekend, with the Dow ultimately closing at a record high.

Jobs: The Miss That Moved Markets

June’s employment report delivered a notable downside surprise. The economy added 57,000 jobs last month, roughly half of the 115,000 economists had forecast and well below May’s 129,000. The immediate market reaction was positive, and the logic is straightforward: a slowing labor market reduces pressure on the Fed to raise rates, pushing back the timeline for any potential hike under Chair Warsh.

The bigger picture is more complicated. Just two months ago, job growth was running well over expectations. The deceleration from May to June is sharp, and whether it reflects a one-month anomaly or the beginning of a more sustained softening will be one of the most important questions markets answer over the next several weeks. A Fed that was already cautious about hiking into slowing growth now has additional reason to hold.

What We’re Watching

Wednesday’s FOMC Minutes

The release of the June meeting minutes will offer the most detailed window yet into how Fed officials, including Chair Warsh, were thinking about the inflation and growth tradeoff at their last meeting. Given that the June jobs report was not yet available at the time of that meeting, the minutes will reflect a Fed that was weighing hot inflation against a still-solid labor market. How that framing compares to this week’s weaker jobs data will shape rate expectations heading into the July meeting.

The Rate Hike Calculus Has Shifted

Three weeks ago, a strong jobs report made a rate hike feel increasingly likely. This week’s miss reverses some of that pressure. Markets will recalibrate the probability of a 2026 hike throughout the week, with the FOMC minutes and Fed officials’ speeches on Thursday as the primary inputs.

Dow at Records, Rotation Continuing

The Dow has now outperformed the Nasdaq in back-to-back weeks and sits at a record high. The rotation from high-multiple tech into cyclicals, financials, and industrials appears to have real staying power. If the jobs slowdown persists, rate-sensitive and dividend-paying sectors could extend their leadership into the summer.

This Week’s Critical Data

- Wednesday: FOMC Minutes (June meeting)

- Thursday: Weekly Jobless Claims; Fed speeches

Source: Investors Business Daily – Econoday economic calendar; July 2, 2026. Forecasts are subject to revision and may not materialize.

As always, if you have any questions about your portfolio or want to discuss your strategy, please don’t hesitate to reach out.

Crescent Private Wealth

Weekly Market Insights

Talk To Us!

Footnotes And Sources

WSJ.com, July 2, 2026

Investing.com, July 2, 2026

CNBC.com, June 29, 2026

WSJ.com, June 30, 2026

CNBC.com, July 1, 2026

WSJ.com, July 2, 2026

WSJ.com, July 2, 2026

Investing involves risks, and investment decisions should be based on your own goals, time horizon, and tolerance for risk. The return and principal value of investments will fluctuate as market conditions change. When sold, investments may be worth more or less than their original cost.

The forecasts or forward-looking statements are based on assumptions, may not materialize, and are subject to revision without notice.

The market indexes discussed are unmanaged, and generally, considered representative of their respective markets. Index performance is not indicative of the past performance of a particular investment. Indexes do not incur management fees, costs, and expenses. Individuals cannot directly invest in unmanaged indexes. Past performance does not guarantee future results.

The Dow Jones Industrial Average is an unmanaged index that is generally considered representative of large-capitalization companies on the U.S. stock market. The Nasdaq Composite is an index of the common stocks and similar securities listed on the Nasdaq stock market and considered a broad indicator of the performance of stocks of technology and growth companies. The MSCI EAFE Index was created by Morgan Stanley Capital International (MSCI) and serves as a benchmark of the performance of major international equity markets, as represented by 21 major MSCI indexes from Europe, Australia, and Southeast Asia. The S&P 500 Composite Index is an unmanaged group of securities that are considered to be representative of the stock market in general.

U.S. Treasury Notes are guaranteed by the federal government as to the timely payment of principal and interest. However, if you sell a Treasury Note prior to maturity, it may be worth more or less than the original price paid. Fixed income investments are subject to various risks including changes in interest rates, credit quality, inflation risk, market valuations, prepayments, corporate events, tax ramifications and other factors.

International investments carry additional risks, which include differences in financial reporting standards, currency exchange rates, political risks unique to a specific country, foreign taxes and regulations, and the potential for illiquid markets. These factors may result in greater share price volatility.