Stocks advanced last week as investors looked past stalled Middle East peace talks and refocused on what ultimately mattered more: a strong corporate earnings season and a Fed decision that, despite historic internal division, kept policy on hold.

The Numbers

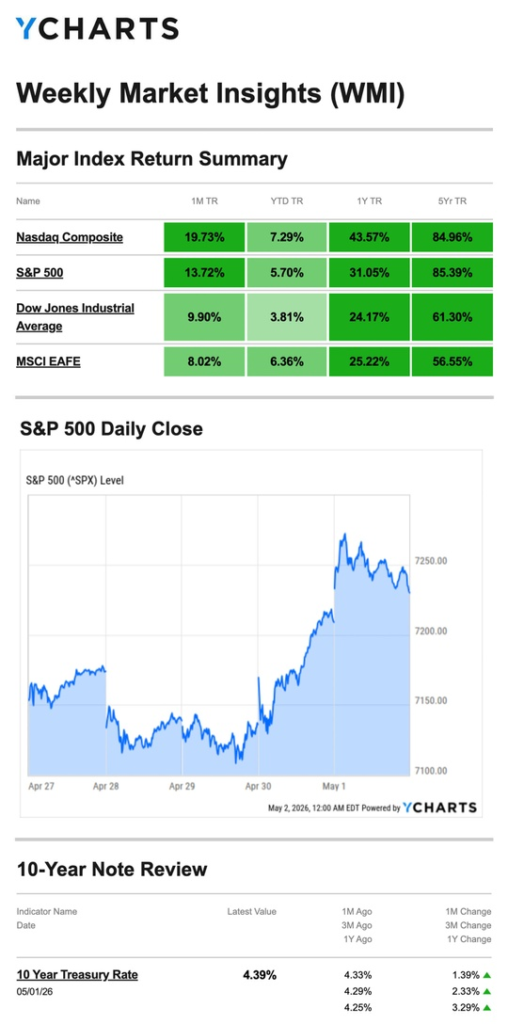

- S&P 500: +0.91%

- Nasdaq: +1.12%

- Dow Jones Industrial Average: +0.55%

- MSCI EAFE: +0.58%

Gains were modest but broad across all four indexes. The weekly numbers, however, undersell the bigger story — both the S&P 500 and Nasdaq closed April with their best monthly performances in five years.

Source: YCharts.com, May 2, 2026. Weekly performance is measured from Monday, April 27, to Friday, May 1. TR = total return for the index, which includes any dividends and cash distributions during the period. Treasury note yield is expressed in basis points.

What Happened

Monday–Tuesday: Peace Talk Frustration, Oil Pressure

Markets opened the week under pressure as progress on Middle East ceasefire negotiations appeared to stall and oil prices climbed. Investor sentiment was cautious heading into a pivotal midweek stretch.

Wednesday: Fed Holds, Earnings Deliver

The Federal Reserve announced it was holding rates steady, as broadly expected — but the vote drew immediate attention. The 8-4 decision was the most divided FOMC vote since 1992, signaling meaningful disagreement among policymakers about the current path. Markets absorbed the news and then shifted focus to the closing bell, when several major companies reported first-quarter results. Investors largely liked what they heard, and stocks rallied to close April on a strong note — with the S&P 500 and Nasdaq each logging their best monthly gain in five years.

Friday: Oil Falls, Megacap Tech Lifts Markets

Stocks extended gains Friday as oil prices retreated and another high-profile megacap technology company reported strong Q1 results. The S&P 500 touched a fresh all-time intraday high.

Fed Leadership: A Transition Takes Shape

Wednesday’s Fed meeting carried significance beyond the rate decision itself. In what was his final FOMC press conference after eight years as Chair, Jerome Powell confirmed he would remain on the Fed’s Board of Governors after his chairmanship expires May 15. Earlier that day, the Senate Banking Committee confirmed Kevin Warsh as the next Fed Chair, with a full Senate confirmation vote still ahead.

The 8-4 vote deserves attention. A divided Fed is not unusual, but a split this wide — the most since 1992 — suggests the four dissenting members may have preferred either a cut or a hike, reflecting genuine disagreement about how to weigh persistent inflation against slowing growth. As Warsh prepares to take the helm, markets will be watching closely for any shift in tone or policy direction under new leadership.

What We’re Watching

Kevin Warsh’s Confirmation and What It Means

Warsh is widely regarded as more hawkish on inflation than Powell. His full Senate confirmation — and any early signals about his policy priorities — will be closely monitored by markets. A more aggressive stance on inflation could push rate cut expectations further out, affecting both bond yields and equity valuations.

Friday’s Jobs Report

The May employment report arrives Friday and will be the week’s most watched release. With the labor market sending mixed signals in recent months — including February’s unexpected job loss and March’s strong rebound — another month of data is needed to establish a clearer trend. The result will also inform how the new Fed leadership inherits the employment picture.

Oil Prices as a Relief Valve

Friday’s pullback in oil prices was a constructive sign. If the ceasefire extension holds and Strait of Hormuz traffic continues to normalize, further declines in energy costs could help bring headline inflation back down — giving the Fed more room and markets more confidence.

This Week’s Critical Data

- Wednesday: ADP Employment Report

- Friday: U.S. Employment Report; Consumer Sentiment

Note: Some releases this week reflect data delayed by last year’s government shutdown. Source: Investors Business Daily – Econoday economic calendar; May 1, 2026. Forecasts are subject to revision and may not materialize.

As always, if you have any questions about your portfolio or want to discuss your strategy, please don’t hesitate to reach out.

Crescent Private Wealth

Weekly Market Insights

Talk To Us!

Footnotes And Sources

WSJ.com, May 1, 2026

Investing.com, May 1, 2026

CNBC.com, April 28, 2026

WSJ.com, April 29, 2026

CNBC.com, April 30, 2026

CNBC.com, May 1, 2026

WSJ.com, April 29, 2026

Investing involves risks, and investment decisions should be based on your own goals, time horizon, and tolerance for risk. The return and principal value of investments will fluctuate as market conditions change. When sold, investments may be worth more or less than their original cost.

The forecasts or forward-looking statements are based on assumptions, may not materialize, and are subject to revision without notice.

The market indexes discussed are unmanaged, and generally, considered representative of their respective markets. Index performance is not indicative of the past performance of a particular investment. Indexes do not incur management fees, costs, and expenses. Individuals cannot directly invest in unmanaged indexes. Past performance does not guarantee future results.

The Dow Jones Industrial Average is an unmanaged index that is generally considered representative of large-capitalization companies on the U.S. stock market. The Nasdaq Composite is an index of the common stocks and similar securities listed on the Nasdaq stock market and considered a broad indicator of the performance of stocks of technology and growth companies. The MSCI EAFE Index was created by Morgan Stanley Capital International (MSCI) and serves as a benchmark of the performance of major international equity markets, as represented by 21 major MSCI indexes from Europe, Australia, and Southeast Asia. The S&P 500 Composite Index is an unmanaged group of securities that are considered to be representative of the stock market in general.

U.S. Treasury Notes are guaranteed by the federal government as to the timely payment of principal and interest. However, if you sell a Treasury Note prior to maturity, it may be worth more or less than the original price paid. Fixed income investments are subject to various risks including changes in interest rates, credit quality, inflation risk, market valuations, prepayments, corporate events, tax ramifications and other factors.

International investments carry additional risks, which include differences in financial reporting standards, currency exchange rates, political risks unique to a specific country, foreign taxes and regulations, and the potential for illiquid markets. These factors may result in greater share price volatility.