Stocks rose for a sixth consecutive week as peace talks progress, better-than-expected jobs growth, and a chipmaker-fueled rally pushed the S&P 500 and Nasdaq to fresh record highs.

The Numbers

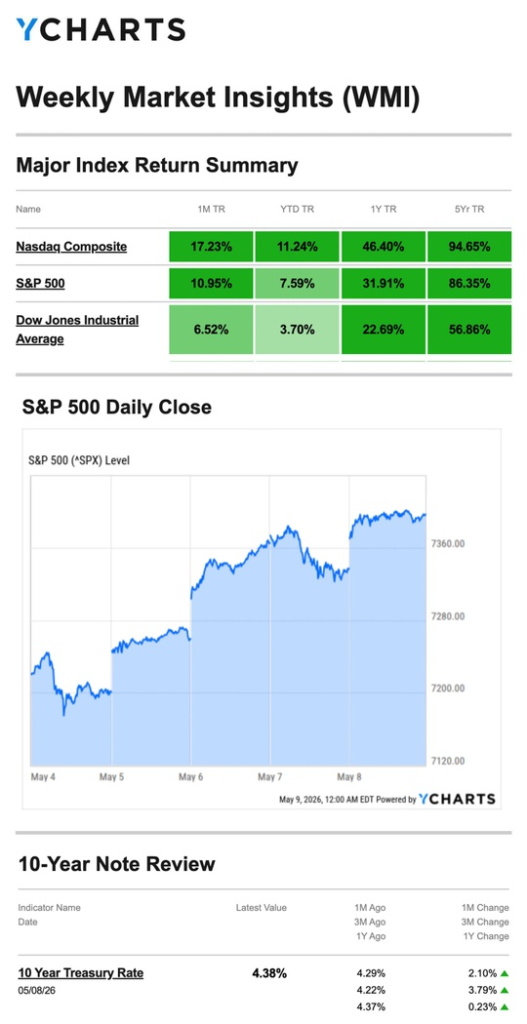

- S&P 500: +2.33%

- Nasdaq: +4.51%

- Dow Jones Industrial Average: +0.22%

- MSCI EAFE: +1.24%

The Nasdaq’s outsized gain reflects a week dominated by semiconductor momentum. The Dow’s modest advance signals that the rally remains concentrated in growth and tech rather than broad cyclical strength.

Source: YCharts.com, May 9, 2026. Weekly performance is measured from Monday, May 4, to Friday, May 8. TR = total return for the index, which includes any dividends and cash distributions during the period. Treasury note yield is expressed in basis points.

What Happened

Monday: Stumble Out of the Gate

Stocks opened the week under pressure as peace negotiations appeared to stall and Middle East tensions ticked higher. The cautious tone didn’t last.

Tuesday–Wednesday: Records Fall

Markets reversed sharply on Tuesday as solid Q1 earnings results and falling oil prices drew buyers back in. Momentum accelerated on Wednesday when stronger-than-expected results from two major chipmakers lifted the entire semiconductor sector and pulled the broader market higher. The S&P 500 and Nasdaq hit record intraday and closing highs on both days, with the S&P closing above 7,300 for the first time.

Thursday: Pause to Assess

Stocks took a brief breather as investors monitored developments in the Middle East. The pause proved temporary.

Friday: Jobs Surprise, Chip Deal, New Highs

Markets opened higher after April’s jobs report came in well above expectations — a relief to investors who had been bracing for conflict-related labor market damage. A major chipmaker acquisition announcement added further fuel, extending the sector’s winning streak and lifting the S&P and Nasdaq to yet another set of record closes, marking six consecutive weeks of gains.

The Data in Focus

Jobs: Better Than Anyone Expected

April’s employment report was a genuine positive surprise. Employers added 115,000 jobs — more than double the 55,000 economists had forecast. Healthcare, retail, and leisure and hospitality led sector growth. The unemployment rate held steady at 4.3%. Perhaps most importantly, the report offered early evidence that the Middle East conflict has not yet meaningfully disrupted U.S. hiring — a concern that had been building for weeks.

Housing: Two Months of Upside

Delayed data on new home sales added another constructive note. March new home sales reached 682,000 units, up 7.4% from February. February’s figure itself was revised higher, showing an 8.9% month-over-month jump. Both months exceeded expectations, suggesting the housing market entered spring with more momentum than many anticipated.

What We’re Watching

Inflation Data Takes Center Stage

Tuesday’s CPI and Wednesday’s PPI arrive at a pivotal moment. Six weeks of equity gains and a strong jobs report have lifted confidence, but inflation running above the Fed’s 2% target remains the central constraint on monetary policy. A cooler reading on either report would reinforce the rally; a hot one would test it.

The Concentration Question

The Nasdaq’s 4.51% gain versus the Dow’s 0.22% advance captures a growing divergence: this rally is being driven heavily by semiconductors and mega-cap tech. Broad market participation would be a healthier sign. Thursday’s retail sales report will offer a read on whether the consumer economy is keeping pace with the tech-driven headline numbers.

Six Weeks and Counting

A six-week winning streak following one of the more turbulent stretches in recent memory is a meaningful development. Whether it reflects a durable fundamental improvement or a relief rally that has run ahead of the underlying reality. It will become clearer as developments in the conflict, inflation data, and Fed signals accumulate in the weeks ahead.

This Week’s Critical Data

- Tuesday: Consumer Price Index (CPI)

- Wednesday: Producer Price Index (PPI)

- Thursday: Retail Sales; Weekly Jobless Claims

Note: Some releases this week reflect data delayed by last year’s government shutdown. Source: Investors Business Daily – Econoday economic calendar; May 8, 2026. Forecasts are subject to revision and may not materialize.

As always, if you have any questions about your portfolio or want to discuss your strategy, please don’t hesitate to reach out.

Crescent Private Wealth

Weekly Market Insights

Talk To Us!

Footnotes And Sources

WSJ.com, May 8, 2026

Investing.com, May 8, 2026

CNBC.com, May 4, 2026

CNBC.com, May 6, 2026

CNBC.com, April 30, 2026

WSJ.com, May 7, 2026

WSJ.com, May 8, 2026

Reuters.com, May 5, 2026

Investing involves risks, and investment decisions should be based on your own goals, time horizon, and tolerance for risk. The return and principal value of investments will fluctuate as market conditions change. When sold, investments may be worth more or less than their original cost.

The forecasts or forward-looking statements are based on assumptions, may not materialize, and are subject to revision without notice.

The market indexes discussed are unmanaged, and generally, considered representative of their respective markets. Index performance is not indicative of the past performance of a particular investment. Indexes do not incur management fees, costs, and expenses. Individuals cannot directly invest in unmanaged indexes. Past performance does not guarantee future results.

The Dow Jones Industrial Average is an unmanaged index that is generally considered representative of large-capitalization companies on the U.S. stock market. The Nasdaq Composite is an index of the common stocks and similar securities listed on the Nasdaq stock market and considered a broad indicator of the performance of stocks of technology and growth companies. The MSCI EAFE Index was created by Morgan Stanley Capital International (MSCI) and serves as a benchmark of the performance of major international equity markets, as represented by 21 major MSCI indexes from Europe, Australia, and Southeast Asia. The S&P 500 Composite Index is an unmanaged group of securities that are considered to be representative of the stock market in general.

U.S. Treasury Notes are guaranteed by the federal government as to the timely payment of principal and interest. However, if you sell a Treasury Note prior to maturity, it may be worth more or less than the original price paid. Fixed income investments are subject to various risks including changes in interest rates, credit quality, inflation risk, market valuations, prepayments, corporate events, tax ramifications and other factors.

International investments carry additional risks, which include differences in financial reporting standards, currency exchange rates, political risks unique to a specific country, foreign taxes and regulations, and the potential for illiquid markets. These factors may result in greater share price volatility.