Stocks extended their winning streak to eight consecutive weeks as optimism over a peace deal, AI enthusiasm, and a new Fed chair taking the helm combined to keep buyers in control despite a choppy start to the week.

The Numbers

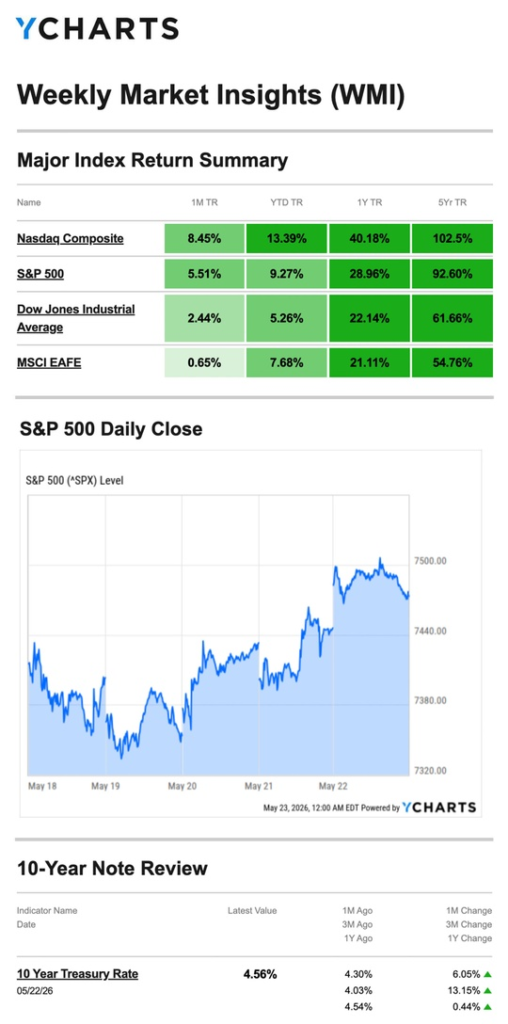

- S&P 500: +0.88%

- Nasdaq: +0.45%

- Dow Jones Industrial Average: +2.13%

- MSCI EAFE: +2.16%

The Dow led U.S. indexes this week, closing at a fresh record high. International developed markets matched the Dow’s momentum, suggesting that optimism over the peace deal is being felt globally. The S&P 500’s eighth straight weekly gain is its longest winning streak since 2023.

Source: YCharts.com, May 23, 2026. Weekly performance is measured from Monday, May 18, to Friday, May 22. TR = total return for the index, which includes any dividends and cash distributions during the period. Treasury note yield is expressed in basis points.

What Happened

Monday: Memory Chip Pressure Weighs on Tech

Stocks stumbled at the open as capacity constraints in the memory chip space, a consequence of surging AI-driven demand, pressured semiconductor stocks and dragged the broader tech sector lower. The AI trade, a consistent source of market momentum in recent weeks, faced its own bout of profit-taking.

Tuesday–Wednesday: Peace Hopes Lift the Dow to a Record

Investor sentiment recovered midweek as renewed optimism around a Middle East peace deal took hold. Oil prices and Treasury yields both fell — a constructive combination for equities. Investors also looked ahead to an earnings report from one of the leading AI chipmakers. The Dow closed at a fresh record high.

Friday: New Fed Chair, New Highs

Markets rallied again to close the week as hopes for a peace deal persisted and enthusiasm for AI and tech broadly remained elevated. Kevin Warsh was officially sworn in as the new Federal Reserve Chair. The Dow posted another record close, and the S&P 500 finished its eighth consecutive week in positive territory.

Fed Minutes: A Rate Hike Is on the Table

The Federal Reserve released minutes from its April FOMC meeting, Jerome Powell’s final meeting as Chair, and the signal buried inside deserves attention.

The minutes indicated that if the Fed were to adjust rates at some point during the remainder of 2026, the adjustment might be a rate hike rather than a cut. That is a meaningful shift in tone from where markets were positioned just a few months ago, when investors were broadly expecting rate reductions. With headline inflation running at a multi-year high driven by energy prices, and a new Fed Chair known for hawkish instincts now at the helm, the possibility of a rate increase is no longer a fringe scenario.

This is the most significant Fed development in months and will likely set the tone for market expectations heading into the summer.

What We’re Watching

Kevin Warsh’s First Moves as Fed Chair

Warsh takes over at a genuinely difficult moment, inflation above target, growth slowing, and a geopolitical situation that has distorted energy markets for months. His early communications and any policy signals will be scrutinized closely. Markets have priced in a patient Fed; any indication of urgency on inflation could quickly reprice that expectation.

Friday’s GDP and PCE

The week’s most consequential data arrives on Friday with the GDP reading and the PCE index. The Fed’s preferred inflation measure. Coming on the heels of the April FOMC minutes signaling a possible rate hike, a hot PCE print would add meaningful weight to the hawkish case. A softer reading would offer some relief.

Peace Deal Watch

Eight weeks of gains have been built in part on the expectation that the Middle East conflict is moving toward resolution. Markets are now pricing in a fair amount of optimism. If peace talks stall or break down, the downside reaction could be swift — particularly given elevated oil prices still embedded in the inflation data.

This Week’s Critical Data

- Thursday: Weekly Jobless Claims; Durable Goods

- Friday: GDP; PCE Index

Note: Investors Business Daily – Econoday economic calendar; May 22, 2026. Forecasts are subject to revision and may not materialize.

As always, if you have any questions about your portfolio or want to discuss your strategy, please don’t hesitate to reach out.

Crescent Private Wealth

Weekly Market Insights

Talk To Us!

Footnotes And Sources

WSJ.com, May 22, 2026

Investing.com, May 22, 2026

CNBC.com, May 18, 2026

CNBC.com, May 20, 2026

CNBC.com, May 21, 2026

WSJ.com, May 22, 2026

WSJ.com, May 20, 2026

IRS.gov, Jan 14, 2026

Investing involves risks, and investment decisions should be based on your own goals, time horizon, and tolerance for risk. The return and principal value of investments will fluctuate as market conditions change. When sold, investments may be worth more or less than their original cost.

The forecasts or forward-looking statements are based on assumptions, may not materialize, and are subject to revision without notice.

The market indexes discussed are unmanaged, and generally, considered representative of their respective markets. Index performance is not indicative of the past performance of a particular investment. Indexes do not incur management fees, costs, and expenses. Individuals cannot directly invest in unmanaged indexes. Past performance does not guarantee future results.

The Dow Jones Industrial Average is an unmanaged index that is generally considered representative of large-capitalization companies on the U.S. stock market. The Nasdaq Composite is an index of the common stocks and similar securities listed on the Nasdaq stock market and considered a broad indicator of the performance of stocks of technology and growth companies. The MSCI EAFE Index was created by Morgan Stanley Capital International (MSCI) and serves as a benchmark of the performance of major international equity markets, as represented by 21 major MSCI indexes from Europe, Australia, and Southeast Asia. The S&P 500 Composite Index is an unmanaged group of securities that are considered to be representative of the stock market in general.

U.S. Treasury Notes are guaranteed by the federal government as to the timely payment of principal and interest. However, if you sell a Treasury Note prior to maturity, it may be worth more or less than the original price paid. Fixed income investments are subject to various risks including changes in interest rates, credit quality, inflation risk, market valuations, prepayments, corporate events, tax ramifications and other factors.

International investments carry additional risks, which include differences in financial reporting standards, currency exchange rates, political risks unique to a specific country, foreign taxes and regulations, and the potential for illiquid markets. These factors may result in greater share price volatility.