Stocks rebounded sharply over a shortened trading week as renewed optimism around a Middle East resolution lifted sentiment — and a surprisingly strong jobs report landed just as markets closed for the holiday.

TThe Numbers

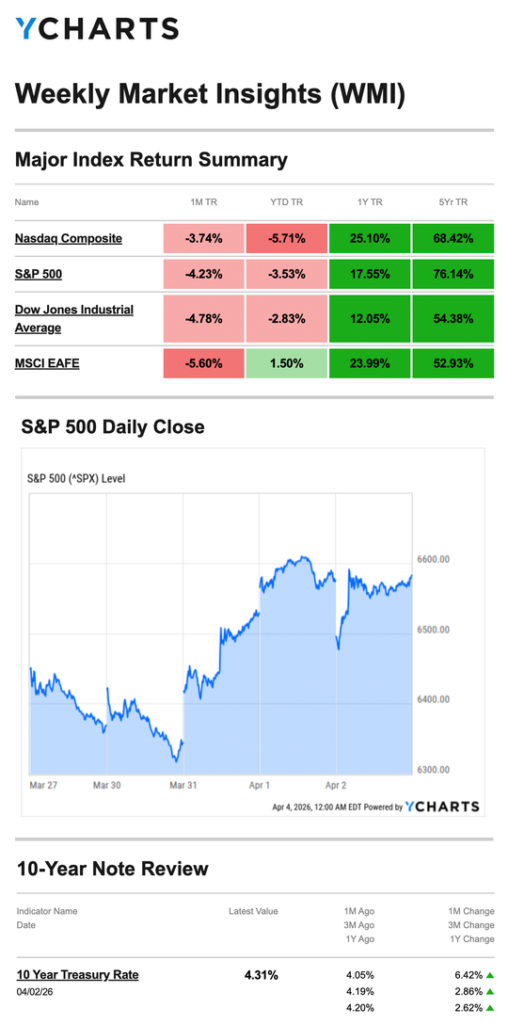

- S&P 500: +3.36%

- Nasdaq: +4.44%

- Dow Jones Industrial Average: +2.96%

- MSCI EAFE: +2.59%

Gains were broad and meaningful across all four indexes, snapping a five-week losing streak for U.S. equities. The Nasdaq led, recouping a significant portion of its recent correction losses in just four sessions.

Source: YCharts.com, April 4, 2026. Weekly performance is measured from Friday, March 27, to Thursday, April 2. TR = total return for the index, which includes any dividends and cash distributions during the period. Treasury note yield is expressed in basis points.

What Happened

Monday: Cautious Start Markets opened under modest pressure. Fed Chair Powell offered measured comments suggesting inflation expectations remain “well anchored beyond the short term” despite the conflict’s potential inflationary effects — a reassuring signal that investors ultimately looked past early in the session.

Tuesday: Q1 Closes on a High Note Sentiment shifted decisively on the final day of the first quarter. Renewed investor confidence in a near-term conflict resolution drove stocks sharply higher, with the S&P 500 posting its best single-day gain since last May. It was a striking turnaround for a quarter that ended under considerable pressure.

Wednesday: White House Comments Add Fuel Momentum carried into Wednesday as White House commentary gave investors additional confidence that a diplomatic resolution was within reach. A stronger-than-expected retail sales report added to the constructive backdrop, keeping buyers engaged.

Thursday: Brief Dip, Then a Breakout Close Stocks pulled back intraday before recovering to finish the session slightly higher — enough to officially end the five-week losing streak that had weighed on portfolios since late February.

Jobs: A Genuine Surprise U.S. markets were closed Friday for the holiday, but the March employment report arrived as scheduled — and it was notably strong. Employers added 178,000 jobs last month, nearly three times the 59,000 economists had forecast and the best monthly gain in over a year. The unemployment rate edged down to 4.3% from 4.4% in February.

This report matters for several reasons. Just one month ago, the economy unexpectedly lost 92,000 jobs. March’s rebound suggests that reading may have been an anomaly rather than the start of a trend — a meaningful distinction for both investor confidence and the Fed’s policy outlook. Markets will have the weekend to digest the number before trading resumes Monday.

What We’re Watching

Can the Rally Hold? Five weeks of losses were erased in four sessions, driven largely by geopolitical optimism. If conflict headlines deteriorate again, the same dynamic that fueled this week’s gains could reverse quickly. The sustainability of this rebound will depend heavily on whether diplomatic progress continues.

A Pivotal Week for Inflation Data This week brings both the PCE index — the Fed’s preferred inflation gauge — on Thursday and the Consumer Price Index on Friday. Coming on the heels of a strong jobs report and rebounding markets, these readings will shape how aggressively the Fed is expected to act (or not act) at its next meeting.

FOMC Minutes on Wednesday The release of March meeting minutes will offer a window into how Fed officials were thinking about the inflation-growth tradeoff before the conflict began to show signs of easing. Any hints about the threshold for rate cuts will be closely parsed.

This Week’s Critical Data

- Thursday: PCE Index (February); Q4 GDP second revision; Weekly Jobless Claims

- Friday: Consumer Price Index (CPI); Consumer Sentiment

Source: Investors Business Daily – Econoday economic calendar; April 3, 2026. Forecasts are subject to revision and may not materialize.

As always, if you have any questions about your portfolio or want to discuss your strategy, please don’t hesitate to reach out.

Crescent Private Wealth

Weekly Market Insights

Talk To Us!

Footnotes And Sources

WSJ.com, April 2, 2026

CNBC.com, March 30, 2026

CNBC.com, March 30, 2026

WSJ.com, March 31, 2026

CNBC.com, April 1, 2026

CNBC.com, April 2, 2026

WSJ.com, April 3, 2026

IRS.gov, October 24, 2025

Investing involves risks, and investment decisions should be based on your own goals, time horizon, and tolerance for risk. The return and principal value of investments will fluctuate as market conditions change. When sold, investments may be worth more or less than their original cost.

The forecasts or forward-looking statements are based on assumptions, may not materialize, and are subject to revision without notice.

The market indexes discussed are unmanaged, and generally, considered representative of their respective markets. Index performance is not indicative of the past performance of a particular investment. Indexes do not incur management fees, costs, and expenses. Individuals cannot directly invest in unmanaged indexes. Past performance does not guarantee future results.

The Dow Jones Industrial Average is an unmanaged index that is generally considered representative of large-capitalization companies on the U.S. stock market. The Nasdaq Composite is an index of the common stocks and similar securities listed on the Nasdaq stock market and considered a broad indicator of the performance of stocks of technology and growth companies. The MSCI EAFE Index was created by Morgan Stanley Capital International (MSCI) and serves as a benchmark of the performance of major international equity markets, as represented by 21 major MSCI indexes from Europe, Australia, and Southeast Asia. The S&P 500 Composite Index is an unmanaged group of securities that are considered to be representative of the stock market in general.

U.S. Treasury Notes are guaranteed by the federal government as to the timely payment of principal and interest. However, if you sell a Treasury Note prior to maturity, it may be worth more or less than the original price paid. Fixed income investments are subject to various risks including changes in interest rates, credit quality, inflation risk, market valuations, prepayments, corporate events, tax ramifications and other factors.

International investments carry additional risks, which include differences in financial reporting standards, currency exchange rates, political risks unique to a specific country, foreign taxes and regulations, and the potential for illiquid markets. These factors may result in greater share price volatility.