Stocks rose over a shortened trading week as the U.S. and Iran reached a peace agreement, oil prices fell sharply, and the Fed held rates steady at Chair Warsh’s first FOMC meeting — delivering the constructive trifecta markets had been waiting months for.

The Numbers

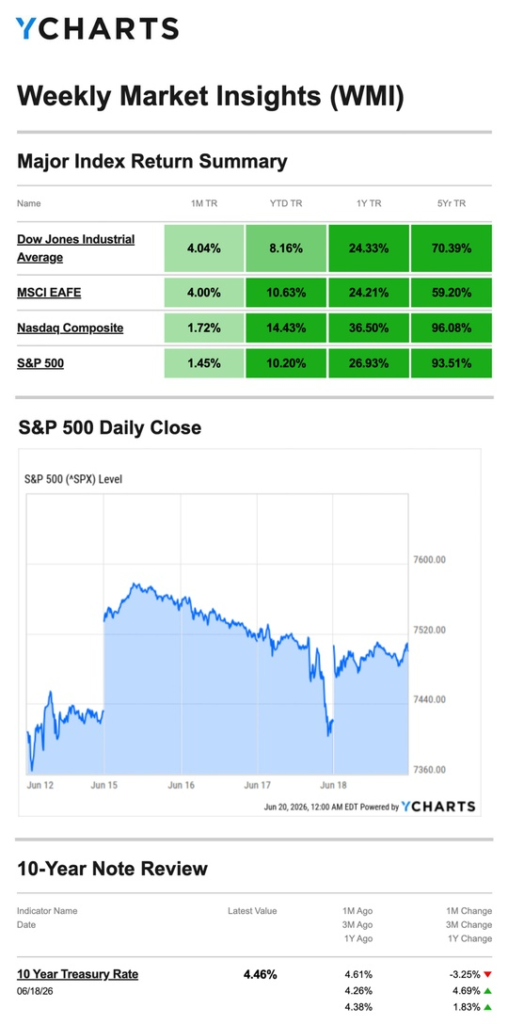

- S&P 500: +0.93%

- Nasdaq: +2.43%

- Dow Jones Industrial Average: +0.71%

- MSCI EAFE: +0.96%

Measured from Friday, June 12, through Thursday’s close. The Nasdaq led as tech stocks recovered from recent selling pressure. The S&P 500 closed out its 11th winning week in the past 12.

Source: YCharts.com, June 20, 2026. Weekly performance is measured from Friday, June 12, to Thursday, June 18. TR = total return for the index, which includes any dividends and cash distributions during the period. Treasury note yield is expressed in basis points.

What Happened

Monday: Peace Deal Moves Markets

The week opened with the most consequential headline of the past several months: the White House announced over the weekend that the U.S. and Iran had reached an agreement. Markets responded immediately. All three major averages climbed between 1% and 3% on Monday, while crude oil prices declined roughly 5%. The kind of simultaneous equity rally and energy pullback investors had been anticipating since the conflict began.

Tuesday: Rotation Takes Hold, Dow Crosses 52,000

Tuesday delivered a split-screen session. The Dow surged to an intraday record, crossing 52,000 for the first time, as falling oil prices boosted banks, industrials, and other cyclical sectors. The S&P 500 and Nasdaq slipped as investors rotated out of tech into those economically sensitive names, a healthy broadening of market participation.

Wednesday: Tech Recovers, Consumer Spending Surprises

Growth stocks bounced back midweek as investors returned to tech ahead of the Fed decision. An unexpected rise in May consumer spending provided additional support and reinforced confidence that the consumer economy remains resilient despite months of geopolitical disruption. Markets entered the Fed announcement in a distinctly risk-on mood.

Thursday: Chipmakers Lead, Winning Streak Extends

Stocks closed the shortened week higher, paced by chipmakers and the broader AI trade. The S&P 500 finished its 11th winning week out of the past 12, a remarkable run given the headwinds markets navigated over that stretch.

Fed Holds Steady — With a Warning

As expected, the Fed kept the federal funds rate unchanged at its 3.50%–3.75% target range at the June meeting. The decision itself was not the story. What mattered was the tone.

In his first press conference as Fed Chair, Kevin Warsh acknowledged the upward drift in inflation this year and reemphasized the Fed’s commitment to its 2% target — language that stopped short of signaling an imminent hike but made clear that the current rate level is not permanent. With headline CPI at 4.2% and core running at 2.9%, Warsh has limited room for patience. Markets interpreted the hold as a reprieve, not a resolution.

What We’re Watching

Thursday’s PCE and GDP

The week’s most important data arrives on Thursday. The PCE index, the Fed’s preferred inflation measure, will offer the first post-peace-deal read on whether energy-driven price pressure is beginning to ease. A softer PCE print would materially reduce the probability of a near-term rate hike and could extend the equity rally. The Q1 GDP revision arrives the same day and will be watched for any further downward movement from the already-soft 1.6% initial estimate.

Oil Price Normalization

Monday’s 5% single-day drop in crude prices was significant. If the peace agreement holds and Strait of Hormuz traffic normalizes over the coming weeks, the energy component driving headline inflation higher could unwind relatively quickly, giving the Fed more room to hold and markets more runway to rally.

The Broadening Rotation

Tuesday’s session, Dow at records while Nasdaq slipped, is worth watching as a pattern. If the rally broadens from growth and tech into cyclicals, financials, and industrials, it suggests investors are gaining confidence in the underlying economy rather than simply chasing momentum. That kind of broad participation tends to be more durable.

This Week’s Critical Data

- Thursday: PCE Index; Q1 GDP Revision; Weekly Jobless Claims; Durable Goods

- Friday: Consumer Sentiment

Source: Investors Business Daily – Econoday economic calendar; June 18, 2026. Forecasts are subject to revision and may not materialize.

As always, if you have any questions about your portfolio or want to discuss your strategy, please don’t hesitate to reach out.

Crescent Private Wealth

Weekly Market Insights

Talk To Us!

Footnotes And Sources

WSJ.com, June 18, 2026

Investing.com, June 18, 2026

CNBC.com, June 15, 2026

CNBC.com, June 16, 2026

WSJ.com, June 17, 2026

CNBC.com, June 18, 2026

WSJ.com, June 17, 2026

Investing involves risks, and investment decisions should be based on your own goals, time horizon, and tolerance for risk. The return and principal value of investments will fluctuate as market conditions change. When sold, investments may be worth more or less than their original cost.

The forecasts or forward-looking statements are based on assumptions, may not materialize, and are subject to revision without notice.

The market indexes discussed are unmanaged, and generally, considered representative of their respective markets. Index performance is not indicative of the past performance of a particular investment. Indexes do not incur management fees, costs, and expenses. Individuals cannot directly invest in unmanaged indexes. Past performance does not guarantee future results.

The Dow Jones Industrial Average is an unmanaged index that is generally considered representative of large-capitalization companies on the U.S. stock market. The Nasdaq Composite is an index of the common stocks and similar securities listed on the Nasdaq stock market and considered a broad indicator of the performance of stocks of technology and growth companies. The MSCI EAFE Index was created by Morgan Stanley Capital International (MSCI) and serves as a benchmark of the performance of major international equity markets, as represented by 21 major MSCI indexes from Europe, Australia, and Southeast Asia. The S&P 500 Composite Index is an unmanaged group of securities that are considered to be representative of the stock market in general.

U.S. Treasury Notes are guaranteed by the federal government as to the timely payment of principal and interest. However, if you sell a Treasury Note prior to maturity, it may be worth more or less than the original price paid. Fixed income investments are subject to various risks including changes in interest rates, credit quality, inflation risk, market valuations, prepayments, corporate events, tax ramifications and other factors.

International investments carry additional risks, which include differences in financial reporting standards, currency exchange rates, political risks unique to a specific country, foreign taxes and regulations, and the potential for illiquid markets. These factors may result in greater share price volatility.