Stocks declined last week as investors wrestled with mixed economic signals and growing concern that AI-driven disruption may be broader — and faster — than previously assumed.

The Numbers

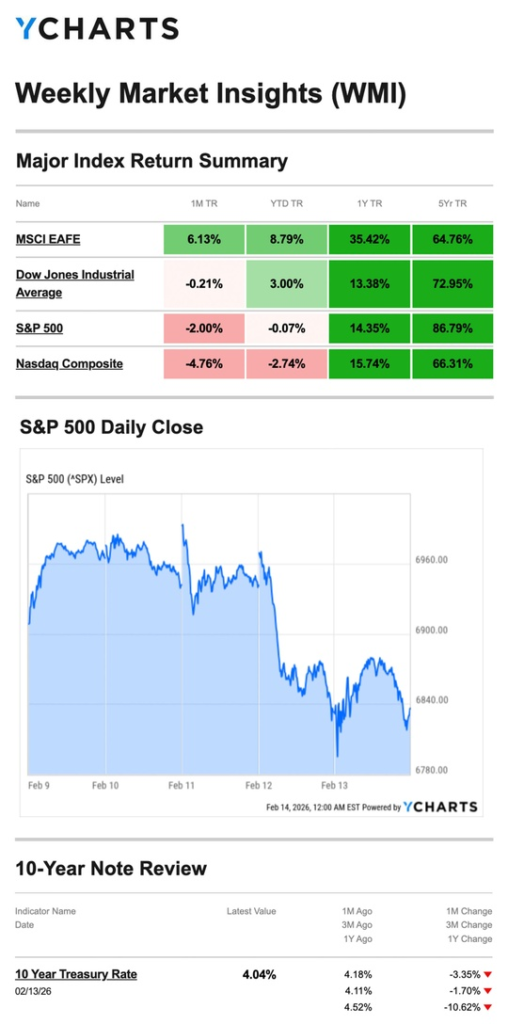

- S&P 500: −1.39%

- Nasdaq: −2.10%

- Dow Jones Industrial Average: −1.23%

- MSCI EAFE: +1.92%

U.S. equities fell across the board, with tech-heavy indexes bearing the brunt of the selloff. International developed markets continued their recent outperformance.

Source: YCharts.com, February 14, 2026. Weekly performance is measured from Monday, February 9, to Friday, February 13. TR = total return for the index, which includes any dividends and cash distributions during the period. Treasury note yield is expressed in basis points.

What Happened

Early Week: Cautious Optimism Markets started the week on firmer footing, with big tech leading the Nasdaq and S&P 500 to modest gains as investors appeared cautiously constructive on the economy and the ongoing Q4 earnings season.

Mid-Week: Mixed Data, AI Anxiety Sentiment shifted Tuesday after December retail sales came in flat — below both expectations and November’s 0.6% growth — raising questions about consumer momentum. Concerns also emerged around AI’s potential impact on financial sector business models.

A stronger-than-expected jobs report briefly sparked a rally midweek, but gains faded quickly as investors parsed the details. Attention then turned to broader AI disruption fears, with traders growing worried that automation could upend business models across multiple industries and contribute to longer-term unemployment pressure.

Late Week: Inflation Offers Relief Markets rebounded Friday after January’s Consumer Price Index (CPI) showed inflation cooling to 2.4% year-over-year — down from 2.7% in December and below expectations. The report gave investors a constructive note to close the week on.

The Data in Focus: Good News / Bad News

Three major economic reports defined the week’s narrative:

Retail Sales Consumer spending was flat in December, missing expectations. The concerning read: two-thirds of U.S. economic activity runs on consumer spending, and the trend is softening. The silver lining: a weaker consumer may give the Fed reason to revisit its current wait-and-see stance on rates.

Employment January job growth came in more than double what economists expected — the strongest gain in over a year — and the unemployment rate edged lower. The concerning read: growth was heavily concentrated in a single sector, and downward revisions revealed employers added only 181,000 jobs in all of 2025 — roughly 70% fewer than originally reported — with essentially no net job growth in the second half of the year.

Inflation January CPI rose 2.4% year-over-year, cooling from December’s 2.7% pace and coming in below forecasts. The concerning read: inflation remains above the Fed’s 2% target, keeping the central bank in a holding pattern.

What We’re Watching

AI Disruption as a Market Force Last week’s selloff was notable because it wasn’t driven by a single earnings miss or a macro shock — it reflected a growing investor reckoning with AI’s potential to reshape entire industries. This theme is unlikely to fade.

A Data-Heavy Week Ahead With markets closed Monday for Presidents’ Day, the week is compressed but packed. Friday brings Q4 GDP and the PCE Index — the Fed’s preferred inflation gauge — making it the most consequential day of the week for rate expectations

This Week’s Critical Data

- Wednesday: FOMC Meeting Notes (January); Durable Goods; Housing Starts

- Friday: Q4 GDP; PCE Index (December); Consumer Sentiment

Note: Several reports reflect delayed publication from the October–November government shutdown.

Source: Investors Business Daily – Econoday economic calendar; February 13, 2026. Forecasts are subject to revision and may not materialize.

As always, if you have any questions about your portfolio or want to discuss your strategy, please don’t hesitate to reach out.

Crescent Private Wealth

Weekly Market Insights

Talk To Us!

Footnotes And Sources

WSJ.com, February 13, 2026

Investing.com, February 13, 2026

CNBC.com, February 9, 2026

CNBC.com, February 10, 2026

CNBC.com, February 12, 2026

WSJ.com, February 13, 2026

CNBC.com, February 10, 2026

WSJ.com, February 11, 2026

WSJ.com, February 13, 2026

IRS.gov, May 29, 2023