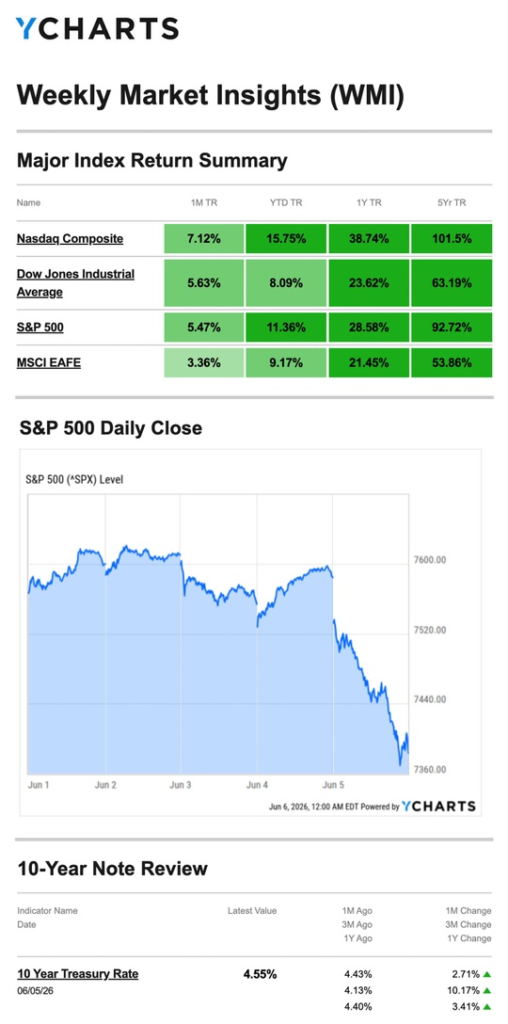

Stocks snapped their nine-week winning streak as a blowout jobs report raised the prospect of a Fed rate hike, while rising oil prices added fresh inflation anxiety to an already fragile market mood.

The Numbers

- S&P 500: −2.59%

- Nasdaq: −4.68%

- Dow Jones Industrial Average: −0.32%

- MSCI EAFE: −1.41%

The Nasdaq bore the brunt of the week’s selling, its worst weekly decline in months, while the Dow held up comparatively well. The divergence reflects a market rotating away from high-valuation, growth stocks in a higher-rate, riskier environment.

Source: YCharts.com, June 6, 2026. Weekly performance is measured from Monday, June 1, to Friday, June 5. TR = total return for the index, which includes any dividends and cash distributions during the period. Treasury note yield is expressed in basis points.

What Happened

Monday–Tuesday: One Last Push to Records

June opened with modest gains as a tech rally absorbed rising oil prices. All three major averages logged new all-time intraday highs and record closes on Monday. The S&P 500 recorded its first close above 7,600 on Tuesday while the Dow advanced nearly half a percentage point. It proved to be the rally’s high-water mark.

Wednesday: Nine-Day Win Streak Snapped

Oil prices climbed further midweek, rekindling inflation concerns tied to the ongoing Middle East situation. The S&P 500 broke its nine-consecutive-day winning streak and, along with the Dow, erased all gains from the start of the week by Wednesday’s close.

Friday: Jobs Report Delivers the Decisive Blow

May’s nonfarm payrolls report came in far stronger than expected, triggering a broad selloff. The S&P fell more than 2.5% on the session, and the Nasdaq dropped more than 4%, its worst single-day performance in recent memory. The mechanism was straightforward: a robust labor market reduces the Fed’s incentive to cut rates and raises the possibility that Chair Warsh may move to hike instead.

Jobs: Too Strong for Comfort

May’s employment report was unambiguously strong — and that created a problem for markets.

The economy added 172,000 jobs last month, more than double the roughly 80,000 economists had expected. Employers appear to have been catching up after a prolonged hiring pause driven by last year’s trade policy uncertainty and federal budget cuts. The unemployment rate held steady at 4.3%. Wednesday’s ADP private-sector report tracked similarly, offering no advance warning of the upside surprise.

In most environments, a strong jobs report is good news. In the current environment — with inflation running above 3%, a new Fed Chair openly considering rate hikes, and oil prices elevated — strong hiring complicates the Fed’s calculus considerably. The market’s reaction on Friday reflected that tension directly.

What We’re Watching

Wednesday’s CPI

This week’s Consumer Price Index is the most important release of the year so far. Coming directly after a jobs report that rattled markets, a hot CPI print would significantly strengthen the case for a Fed rate hike. A cooler reading could help stabilize sentiment and give Chair Warsh room to hold steady. There is little middle ground this week — the number will move markets.

Thursday’s PPI

Wholesale inflation data arrives the day after CPI, completing a two-day inflation picture. With PPI already running at a three-year high as of April, another elevated reading would reinforce the pressure building on the Fed to act.

The Rate Hike Conversation

Just weeks ago, markets were debating the timing of rate cuts. That conversation has now shifted to whether a rate hike is coming. The speed of that shift — driven by sticky inflation, a strong labor market, and a new Fed Chair with hawkish instincts — is itself a significant market development. How investors reprice risk assets in a potential hiking environment will be the defining story of the summer.

This Week’s Critical Data

- Wednesday: Consumer Price Index (CPI)

- Thursday: Producer Price Index (PPI); Weekly Jobless Claims

- Friday: Consumer Sentiment

Note: Investors Business Daily – Econoday economic calendar; June 5, 2026. Forecasts are subject to revision and may not materialize.

As always, if you have any questions about your portfolio or want to discuss your strategy, please don’t hesitate to reach out.

Crescent Private Wealth

Weekly Market Insights

Talk To Us!

Footnotes And Sources

WSJ.com, June 5, 2026

Investing.com, June 5, 2026

CNBC.com, June 1, 2026

CNBC.com, June 3, 2026

CNBC.com, June 4, 2026

WSJ.com, June 5, 2026

WSJ.com, June 5, 2026

Investing involves risks, and investment decisions should be based on your own goals, time horizon, and tolerance for risk. The return and principal value of investments will fluctuate as market conditions change. When sold, investments may be worth more or less than their original cost.

The forecasts or forward-looking statements are based on assumptions, may not materialize, and are subject to revision without notice.

The market indexes discussed are unmanaged, and generally, considered representative of their respective markets. Index performance is not indicative of the past performance of a particular investment. Indexes do not incur management fees, costs, and expenses. Individuals cannot directly invest in unmanaged indexes. Past performance does not guarantee future results.

The Dow Jones Industrial Average is an unmanaged index that is generally considered representative of large-capitalization companies on the U.S. stock market. The Nasdaq Composite is an index of the common stocks and similar securities listed on the Nasdaq stock market and considered a broad indicator of the performance of stocks of technology and growth companies. The MSCI EAFE Index was created by Morgan Stanley Capital International (MSCI) and serves as a benchmark of the performance of major international equity markets, as represented by 21 major MSCI indexes from Europe, Australia, and Southeast Asia. The S&P 500 Composite Index is an unmanaged group of securities that are considered to be representative of the stock market in general.

U.S. Treasury Notes are guaranteed by the federal government as to the timely payment of principal and interest. However, if you sell a Treasury Note prior to maturity, it may be worth more or less than the original price paid. Fixed income investments are subject to various risks including changes in interest rates, credit quality, inflation risk, market valuations, prepayments, corporate events, tax ramifications and other factors.

International investments carry additional risks, which include differences in financial reporting standards, currency exchange rates, political risks unique to a specific country, foreign taxes and regulations, and the potential for illiquid markets. These factors may result in greater share price volatility.